Floor Plan Financing Bonus Depreciation

Kbkg Tax Insight Impact Of Bonus Depreciation For Companies With Floor Plan Financing Kbkg

2019 Bonus Depreciation Update For Auto Dealers Councilor Buchanan Mitchell Cbm

Bonus Depreciation Rules Favor Dealerships With Floor Plan Financing Interest 2019 Articles Resources Cla Cliftonlarsonallen

Product Page Skyline Homes Floor Plans Manufactured Homes Floor Plans Modular Home Plans

Thank You Factory Tour The Home Store Modular Home Floor Plans Two Story House Plans Pole Barn House Plans

2 Storey House Plans Floor Plan With Perspective New Nor Cape House Plans House Plans 2 Storey House Layout Plans

Taxpayers that have assets used in regulated utilities or that have had floor plan financing interest also received specific guidance in the 2019 proposed regulations.

Floor plan financing bonus depreciation. As long as the dealership does not need to use the floor plan interest exception to fully deduct business interest including floor plan interest then the dealership is still eligible to take advantage of the favorable full expensing provisions of. Through some tax planning the automobile dealership decides the new construction location will be owned by a new real estate holding company. Dealerships that take the floor plan financing interest exclusion in computing their limit can t claim 100 bonus depreciation for their fixed asset additions. Specifically the 2019 proposed regulations address the following.

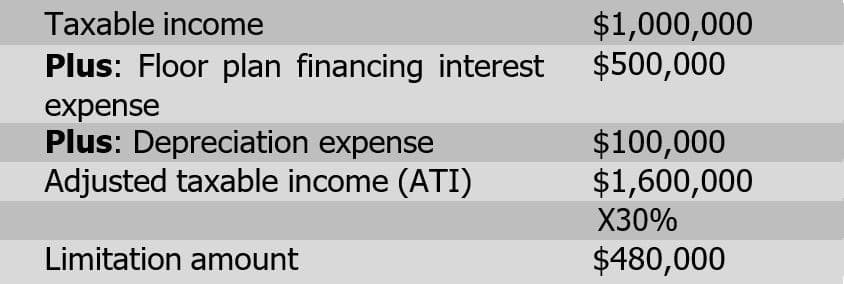

This leads to an unexpected trade off. Fortunately the recent proposed regulations clarified three key elements of the interaction between the interest expense and bonus depreciation rules. Any business that deducts floor plan financing interest cannot claim bonus depreciation on any property acquired by that trade or business. 10 30 2019 under the tax reform rules passed in 2017 the deduction for net business interest expense was generally limited to 30 of a dealership s adjusted taxable income plus 100 of floor plan financing interest expense.

The tax cuts and jobs act of 2017 tcja increases the bonus depreciation rate from 40 to 100 for property acquired after sept. Floor plan interest remains fully deductible but interest expense on debt other than floor plan financing debt may be limited due to 1 and 2. The tcja also made changes to the bonus depreciation rules including increasing the percentage from 50 to 100 and excluding certain properties from bonus depreciation eligibility. Tax strategies bonus depreciation rules favor dealerships with floor plan financing interest.

Floor plan financing interest expense remained fully deductible under tax reform. This planning opportunity paired. The proposed regulations provide for a special rule applicable to taxpayer with floor plan interest determining when it is taken into account for purposes of the 163 j business interest limitations. Auto dealers with floor plan financing interest are still eligible for bonus depreciation.

27 2017 and placed into service after dec. But it came at a cost. The automobile dealership operating company benefits from floor plan financing so bonus depreciation will not apply to assets placed into service by the company in 2019. If such interest was initially considered floor plan financing interest then most auto dealers would be prohibited from taking the accelerated deductions for 100 bonus depreciation.

As a result virtually no auto dealers will be able to take advantage of the expanded bonus depreciation provisions of the tcja.

The Taylor House Plans First Floor Plan Ideas For Kitchen Into Great Room Floor Plans House Plans Garage Plans Detached

Plan 89988ah 3 Bed Craftsman Ranch With Open Concept Floor Plan Floor Plans Ranch Open Concept Floor Plans Ranch House Plans

Cypress Iii Floor Plan Bluestone Eastwood Homes Floor Plans How To Plan Richmond Homes

Plan 33117zr Net Zero Energy Saver House Plan Mediterranean House Plans House Plans Ranch House Plans

Plan 17801lv Stunning Open Floor Plan New House Plans Best House Plans Open Floor Plan

The Mcmillan Floor Plan Signature Collection Basement Floor Plans Rambler House Plans Basement House Plans

3 Bedroom Floor Plan C 9810 Hawks Homes Manufactured Modular Conway Little Rock Arkansas Bedroom Floor Plans Floor Plans 3 Bedroom Floor Plan

Ranch Style House Plan 3 Beds 2 Baths 1796 Sq Ft Plan 70 1243 Ranch Style House Plans Best House Plans Ranch House Plans

Plan 765011twn 5 Bed Beach Y House Plan With Two Upstairs Options Included House Plans Pier And Beam Foundation Architectural Design House Plans

Highland Homes Shennandoah Ii Floor Plans Highland Homes How To Plan

Plan 69554am 3 Bedroom Craftsman Ranch Home Plan Floor Plans Ranch Craftsman Ranch Craftsman House Plans

Laundry Craft Room Floor Plans Google Search Garage House Plans Bedroom Floor Plans Garage Floor Plans

Details Template Mobile Home Floor Plans Triple Wide Mobile Homes Modular Home Plans